Want to know more?

In essence, ATAD3 imposes increased reporting obligations and denial of tax benefits under double tax treaties and EU Directives for entities who are considered ‘Shell Companies’.

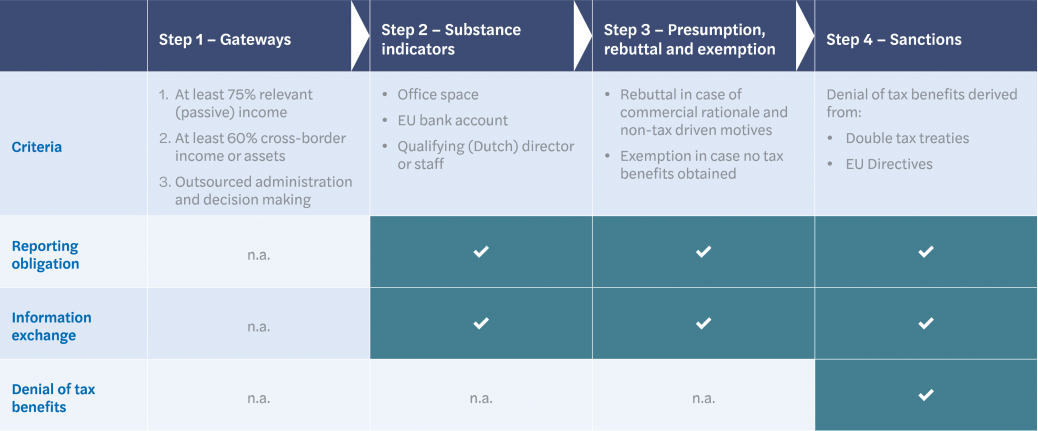

To identify whether ATAD3 applies to your company, the following step plan applies:

A company is considered a ‘shell’ if, in the preceding two tax years, it meets the following three criteria or ‘Gateways’:

Certain exemptions apply where the ‘Gateways’ do not trigger reporting obligations. In summary, these exemptions include certain:

If an entity passes the three ‘Gateways’, it would be obliged to report whether it meets the following three substance indicators:

Not meeting the substance indicators results in the automatic exchange of certain information between EU Member States.

If an entity does not meet all substance indicators or does not provide sufficient supporting evidence, it is assumed that the entity has no minimum substance and is therefore a ‘Shell Company’. However, there is a rebuttable presumption. An entity may provide additional evidence, for example by showing that there are commercial and non-tax driven reasons for its establishment in an EU Member State, and may therefore argue that it should not be regarded as a ‘Shell Company’.

An EU Member State shall treat an entity as having rebutted the presumption if the evidence that the entity has provided proves that the entity has performed and continuously had control over, and borne the risks of, the business activities that generated the relevant income or, in the absence of income, the entity’s assets.

The following tax consequences apply to ‘Shell Companies’:

In essence, ATAD3 aims to ignore the Shell Company’s existence for tax purposes in a number of situations and may allow EU Member States to impose penalties when reporting obligations have been violated.

If adopted, ATAD3 should be implemented into national legislation of the EU Member States by 30 June 2023, and come into effect by 1 January 2024. Since the ‘Gateways’ use a reference period of the two previous tax years, this reference period may have already started for your organization.

ATAD3 can only be adopted by unanimity. It is not yet clear whether the EU Member States will easily reach an agreement on ATAD3 in its current form. Nonetheless, it is critical to assess the implications of ATAD3 for your international tax structure and act now to avoid adverse tax consequences in the future.

International real estate structures, holding structures and financial investment structures could be impacted by ATAD3. Especially if they have outsourced the day-to-day administration and decision-making. As a result, tax benefits under double tax treaties and EU Directives may be denied. Mazars closely monitors the developments regarding ATAD3 and is happy to review your structure(s) in light of ATAD3.

Do you want to know more about the impact of ATAD3 for your current operations and structure(s)? Please contact Erik Stroeve via email or by phone +31 (0)88 277 24 55 or Arno van der Wijk via email or by phone +31 (0)88 277 24 33. They can help you further.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.