7 April 2023 - The Dutch government published changes to the application of the exemption method for directors' fees of statutory directors and supervisory directors abroad.

In general, the income of statutory directors and supervisory directors (further: directors), residents of the Netherlands, is taxed in the country where the company is situated.

In order to avoid double taxation, most tax treaties apply the credit method. This means that the tax paid abroad is deducted from the personal income tax due in the Netherlands on the worldwide income (including the directors’ fee).

This may result in an additional amount of Dutch tax in case the tax paid abroad is less than the tax due in the Netherlands.

Based on a Decree of the State Secretary of Finance published in 2008, directors could apply the exemption method in relation to their directors’ fee in their Dutch personal income tax returns, under the following conditions:

The board members’ remuneration is actually subject to taxation in the foreign country;

and in the foreign country there isn’t a more favourable regime for such income than for a standard employment income.

The exemption method consists of a reduction of the Dutch personal income tax due. In short, the reduction is calculated as follows:

Foreign income / worldwide income * income tax due on worldwide income

The outcome of this calculation is the reduction of the tax due in the Netherlands on the worldwide income. In case the reduction calculated is higher than the amount of tax paid abroad, which is usually the case, there is an advantage when applying this method.

On July 13, 2022 the State Secretary announced that the above possibility will be abolished per January 2023. As a result, directors will no longer be able to use the exemption method, but the credit method will apply as of 1 January 2023.

As a result of this change, directors residing in the Netherlands and performing activities as a director of a foreign company may receive a lower net fee for their director’s activities.

To clarify the tax consequences, you will find an example below.

Example

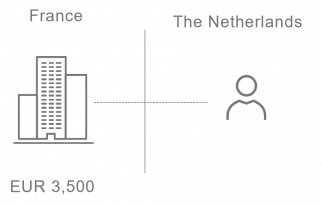

A Dutch resident is a board member of company X, which is established in France. This board member receives an annual remuneration of €25,000. This remuneration is effectively taxed in France at a rate of 14%, which is similar to French wage tax rate. Therefore, the Dutch conditions for granting a tax reduction using the exemption method are met. This means that the Dutch board member only pays an amount of €3,500 (€25,000 x 14%) of French personal income tax and no personal income tax in the Netherlands.

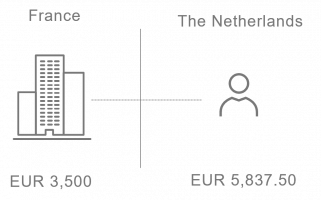

The repeal of the Dutch tax policy, announced by the State Secretary on 13 July 2022, will lead to a different outcome as of 1 January 2023. Consequently, the tax relief granted by the Netherlands will be based on the credit method. This relief consists of a deduction of the French taxes due on the total amount of the Dutch personal income tax due on the remuneration. In this way, the Dutch board member of the French company will be taxed in the same manner as a Dutch board member of a Dutch company. The total amount of Dutch personal income tax due on the remuneration is €9,337.50 (€25.000 x 37,35%). This amount is reduced by the personal income tax paid in France (€3,500 (€25,000 x 14%)), resulting in an amount of €5,837.50 of Dutch personal income tax due.

This example shows that based on the previous Dutch tax policy, the Dutch board member of a French company will pay a total amount of €3,500 of personal income tax. As of 1 January 2023, the Dutch board member will have to pay both French and Dutch personal income tax, resulting in a total amount of €9,337.50.

Want to know more?

Do you want to know more about the impact of this changes? Please contact Alexander Rasink via email or by phone +31 (0)88 277 1615 or Madelon Warning via email or by phone +31 (0)88 277 2426. They can help you further.

24 March 2022 – The Advocate General (A-G) of the Court of Justice of the European Union (CJEU) has concluded the following in two cases: if foreign temporary workers have no work in the Netherlands between two employment contracts the social security legislation of the state of residence applies. This conclusion may be of importance to Dutch temporary employment agencies that employ workers who temporarily...

Deploying staff on global assignments can create escalating challenges for managing the risks arising from in tax, social security, immigration, payroll and corporation tax considerations. To be able to respond to these challenges, global mobility policies and processes often need to be implemented and / or reviewed from several different areas of expertise. This complex future demands flexible solutions...

Do you perform fiscal activities abroad or are you a working expat? Then you have to deal with complex international regulations. Do you know which tax regulations you must comply with? The specialists from Mazars can help you with this. They explain the tax implications of your international activities clearly, so that you can maximise the opportunities for your business.

Income tax is a taxation levied on natural persons on income from employment, such as profits from business activities, but also on income from home ownership, pension and annuity benefits, income from substantial interest and income from savings and investments.