ATAD3 in a Nut-"Shell”

In essence, ATAD3 imposes increased reporting obligations and denial of tax benefits under double tax treaties and EU Directives for entities who are considered ‘Shell Companies’.

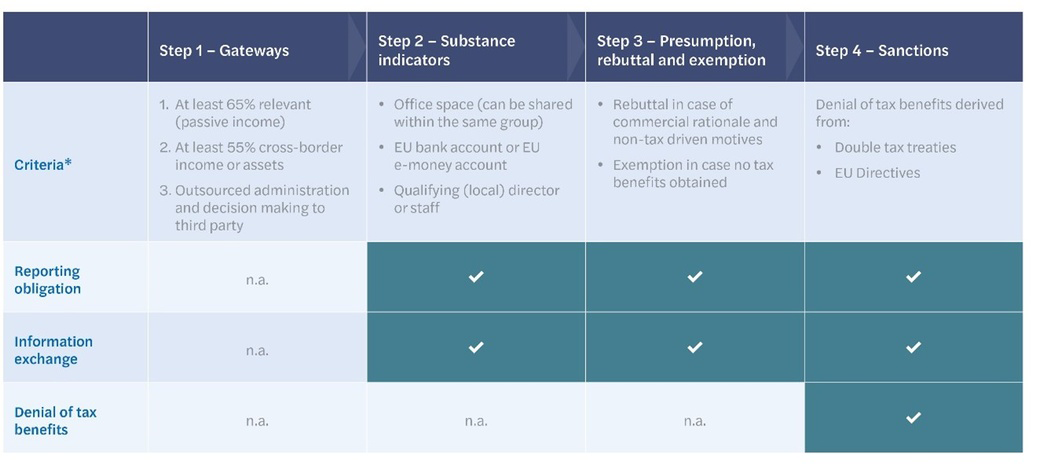

To identify whether ATAD3 applies to you, the following approach applies:

- Gateways: Identify whether a company is a shell or not. Typically, the case when management and administration are outsourced in international groups.

- Substance indicators: Shell Companies must annually report whether minimum substance requirements are met.

- Presumption and rebuttal: Not meeting the minimum substance requirements results in the presumption of lack of substance. This presumption can be rebutted by providing additional information to the local tax authorities on the substance.

- Sanctions: If the presumption is not rebutted, EU tax benefits and tax treaty benefits are denied to the Shell Company.

* Proposed amendments are included in this table

For a more general outline of ATAD3 and the relevant steps, we refer to this article.

Proposed amendments

The proposed amendments of the European Parliament seek to establish a further framework to combat the misuse of Shell Companies. In some ways, it broadens the scope for application of ATAD3, while simultaneously the amendments provide more possibilities to demonstrate substance. We have summarized the most significant changes below.

Step 1 - Gateways

The European Parliament proposes to reduce the thresholds of Gateways one and two. To be considered a Shell Company, the following amendments are being proposed:

- The company must have at least 65% (previously 75%) relevant passive income; and

- More than 55% (previously 60%) of the income / investments are cross-border or 55% (previously 60%) of the assets are located outside the entity’s state of residence.

Additionally, it is proposed that an entity only meets the third gateway if it outsources its administration and decision-making to a third party. Outsourcing these functions to an associated company will no longer trigger the application of ATAD3. Generally, companies are regarded as associated in the case of an (in)direct ownership relation of at least 25%.

Whilst included in the initial draft Directive, companies with at least five employees generating passive income are proposed to be no longer exempted from the increased reporting obligations of ATAD3.

Step 2 - Substance indicators

The proposed amendments seem to ‘relax’ ATAD3’s minimum substance requirements.

Under the proposed amendments, office spaces can be shared with companies within the same group and bank accounts held through e-money institutions in the EU contribute to demonstrating substance.

Opposed to the initial draft Directive, local resident directors may be employed by third parties and perform directorships for non-associated companies.

Step 3 - Presumption and rebuttal

The proposed amendments stipulate that Member States should consider a request to rebut the presumption of lack of substance within nine months of the submission of the application. This request is considered to be accepted in the absence of an answer from the Member State after the expiry of this nine-month period.

Step 4 - Sanctions

ATAD3’s proposed revisions also address the consequences of being treated as a Shell Company. If adopted, Member States will have to justify the refusal of a tax residency certificate in an official statement, increasing the administrative burden on local tax authorities.

What’s next?

The amendments proposed by the European Parliament will be included into ATAD3 as non-binding recommendations. If adopted, ATAD3 should be implemented into national legislation of the EU Member States by 30 June 2023, and come into effect by 1 January 2024. The (expected) one-year deferral to 1 January 2025 has not been included in the non-binding recommendations.

ATAD3 requires unanimity for adoption. It is not yet clear whether all Member States will reach an agreement on ATAD3 and in what form it will be implemented. Nonetheless, it is critical to assess the implications of ATAD3 for your international tax structure and act now to prevent adverse tax consequences moving forward. Since the Gateways use a reference period of the two previous tax years, this reference period has already started for your organisation.

Impact on your real estate structure or financial investment structure

International real estate structures, holding structures and financial investment structures, could be impacted by ATAD3. Especially, if they have outsourced the day-to-day administration and decision-making to a third party. Consequently, tax benefits under double tax treaties and EU Directives may be denied. Mazars closely monitors the developments regarding ATAD3 and is happy to review your structure in light of ATAD3.

Want to know more?

Want to know more about the impact of ATAD3 for your current operations and structure? Please feel free to contact us. Please contact Erik Stroeve by email or by telephone +31 (0)88 277 24 55 or Arno van der Wijk by email or by telephone +31 (0)88 277 24 33. They will be happy to help you.